The Economics of Wi-Fi 7 CPE: Cost, Refresh Cycles, and Operator ROI

Beyond Speed: The Financial and Strategic Stakes of Wi Fi 7 for Operators

7 Minute Read

Wi-Fi 7 promises multi-gigabit performance, lower latency, and a more deterministic wireless experience — but for operators, the transition is far more than a technical upgrade. It is a financial decision that affects capital planning, operational efficiency, customer satisfaction, and competitive positioning. As broadband markets accelerate toward multi-gig speeds, the economics of CPE will shape operator strategy for the next decade.

CPE — gateways, routers, mesh nodes, ONTs, and fixed wireless gateways — represents one of the largest recurring investments for broadband providers. Poor in-home Wi-Fi remains the top driver of customer complaints, meaning CPE directly influences both cost and experience. With Wi-Fi 7 entering the mainstream, operators will need to evaluate not only performance gains but also the economic implications of higher hardware complexity, compressed refresh cycles, and rising customer expectations. The broader CPE market underscores this urgency. Global Wi-Fi CPE revenues are projected to grow from $12.4 billion in 2024 to $25.6 billion by 2033, driven by multi-gig broadband adoption, smart home expansion, and enterprise digitization. Wi-Fi 7 sits at the center of this growth, making its economics impossible for operators to ignore.

Wi-Fi 7 introduces architectural requirements that significantly increase the bill of materials compared to Wi-Fi 6 and 6E. Modern gateways must support three bands — 2.4 GHz, 5 GHz, and 6 GHz — and advanced features such as 320 MHz channels and Multi-Link Operation. These capabilities require more antennas, additional RF chains, and more complex PCB layouts. Higher throughput and 4096-QAM (4K-QAM) demand more powerful processors, larger RAM, and expanded flash storage. As cloud-managed Wi-Fi, analytics, and remote diagnostics become standard, software footprints grow, pushing operators toward higher-end SoCs. These performance gains also generate more heat, requiring improved thermal design and larger enclosures.

Even though Automated Frequency Coordination is still rolling out, CPE must be built to support it, adding certification and hardware requirements. Combined with elevated silicon pricing and lingering supply chain pressures, Wi-Fi 7 CPE typically costs 30-60% more than comparable Wi-Fi 6 hardware. Software complexity adds another layer. AI-driven optimization, SDN/NFV integration, remote firmware automation, and mandatory cybersecurity compliance — especially in North America, Europe, and APAC — increase development and certification costs. These requirements further push memory and processing needs, raising overall CPE cost. Operators historically refreshed CPE every five to seven years. Wi-Fi 7 disrupts this pattern. As operators introduce 2 Gbps, 5 Gbps, and even 10 Gbps broadband tiers, older Wi-Fi 5 and Wi-Fi 6 gateways become bottlenecks inside the home. Customers increasingly judge broadband quality by Wi-Fi performance, not access network capability. With dozens of connected devices per household, older CPE struggles with latency, scheduling, and multi-device handling. Competitive pressure accelerates the cycle further. Once one operator launches Wi-Fi 7 CPE, others must follow to avoid churn — especially in markets where fiber and fixed wireless compete directly. As Wi-Fi 7-capable phones, laptops, and TVs proliferate, customers expect their home Wi-Fi to match device capabilities. Mesh systems complicate the picture. Poor placement, legacy backhaul, and mixed client environments degrade performance and drive support calls, often forcing earlier replacements. As a result, refresh cycles may shrink to three or four years, increasing capital pressure.

Regional dynamics also matter. North America and Western Europe tend to adopt premium Wi-Fi earlier, while APAC and LATAM remain more cost-sensitive, creating staggered upgrade waves. Operators must align refresh strategies with regional economics, device penetration, and competitive intensity. Despite higher costs, Wi-Fi 7 can deliver strong returns when deployed strategically. Wi-Fi 7 enables operators to introduce multi-gig fiber plans and premium Wi-Fi bundles. These offerings justify higher monthly fees and increase ARPU. 'Pro Wi-Fi' and 'Whole Home Wi-Fi' packages become easier to monetize when backed by deterministic performance and 6 GHz capacity. Better in-home performance reduces call center volume, truck rolls, and customer frustration. Since most support calls originate from Wi-Fi issues, improved CPE performance directly lowers operational expenditure. Superior Wi-Fi experience increases customer satisfaction and retention — especially in competitive markets where switching barriers are low. Even a modest reduction in churn carries outsized value, since winning back a lost subscriber typically costs far more than retaining an existing one.

Wi-Fi 7's deterministic scheduling and high-density capabilities strengthen managed Wi-Fi offerings for retail, warehouses, hospitals, and campuses. For SMEs, Wi-Fi 7 CPE with AI-driven management, SD-WAN, and SASE integration opens new monetization paths. FWA providers benefit even more. Wi-Fi 7 helps offset radio variability by improving in-home performance, stabilizing customer experience and reducing churn. Several risks can dilute the economic benefits of Wi-Fi 7. Legacy devices can limit perceived performance gains, creating customer confusion and driving additional support calls. Low 6 GHz device penetration means many users will not immediately experience the full advantages of Wi-Fi 7, reducing early satisfaction. Mesh placement issues continue to undermine backhaul quality and overall performance, often increasing operational overhead. Uncertainty around AFC complicates planning for 6 GHz outdoor and standard-power deployments, while operator-funded CPE subsidies add financial pressure during large-scale upgrades. In addition, regulatory fragmentation across regions — particularly in Europe, APAC, and MEA — makes certification, SKU management, and supply chain coordination more complex. Operators must address these risks proactively to protect ROI.

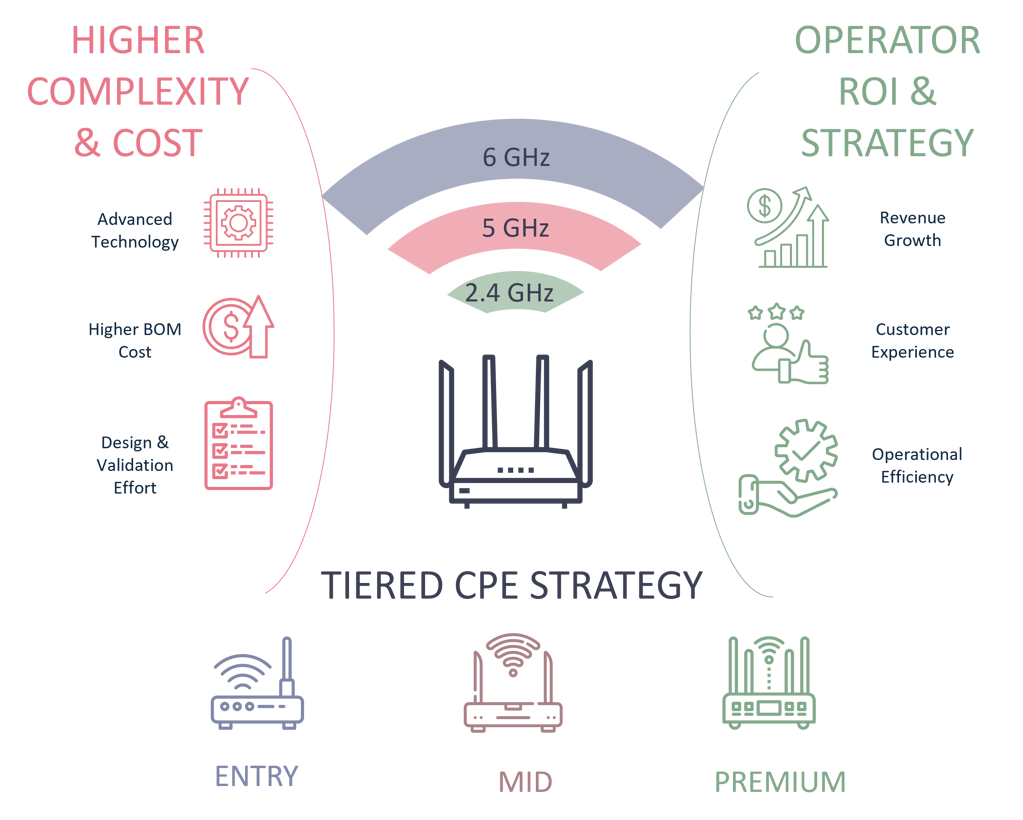

A tiered CPE strategy allows operators to reserve Wi-Fi 7 for multi-gig plans while using Wi-Fi 6 for basic tiers. Premium mesh systems can be offered as upsells. Clear customer education around device compatibility, 6 GHz benefits, and mesh placement best practices reduces support calls and improves satisfaction. SON and analytics tools help optimize performance and reduce operational overhead. Smarter refresh cycles — targeting high-value or high-impact segments first — prevent unnecessary blanket upgrades. On the enterprise side, bundling Wi-Fi 7 with SD-WAN, SASE, or private 5G expands revenue opportunities. Regional go-to-market strategies matter as well. North America favors premiumization and subscription models, Europe emphasizes sustainability and compliance, APAC demands cost-optimized variants, and LATAM/MEA require localized financing and distribution strategies.

The current generation of wireless technology is not the endpoint. Wi‑Fi 8 (IEEE 802.11bn) is expected to introduce multi‑AP coordination, deterministic scheduling, AI‑driven MAC enhancements, and deeper integration with 5G and 6G. To avoid stranded assets and ensure a smooth evolution, operators need to treat today’s investments as part of a longer convergence path. With the global CPE market projected to nearly double by 2033, those who align their upgrade roadmaps with long‑term market growth will be best positioned to capture value across residential, SME, and enterprise segments.

The shift to next‑generation Wi‑Fi also reshapes the financial landscape for operators. Higher CPE costs, compressed refresh cycles, and rising customer expectations introduce new economic pressures — yet the potential ROI remains compelling. Strategic deployment, strong customer education, and forward‑looking planning for Wi‑Fi 8 can collectively unlock superior broadband experiences while preserving healthy economics. This transition is ultimately about more than faster wireless speeds; it is about building a CPE strategy resilient enough to survive the move into the next standard. The immediate, practical decision is clear: define which subscriber tiers and segments receive the new generation of CPE first, rather than defaulting to a blanket upgrade.